HomeDebt Advice HubarticlesStruggling with a Limited Company BTL Mortgage? 2026 Criteria, Personal Guarantees & Your Assets

Struggling with a Limited Company BTL Mortgage? 2026 Criteria, Personal Guarantees & Your Assets

Articles

For many UK property investors, purchasing through a corporate structure was pitched as a strategy to build a resilient business. But when cash flow dries up, interest rates bite, or tenant arrears mount, a harsh reality sets in. Too many directors are told that a limited company completely shields their personal life from business risk.

It doesn’t. A mortgage isn’t just a number on paper; it’s the weight of every room.

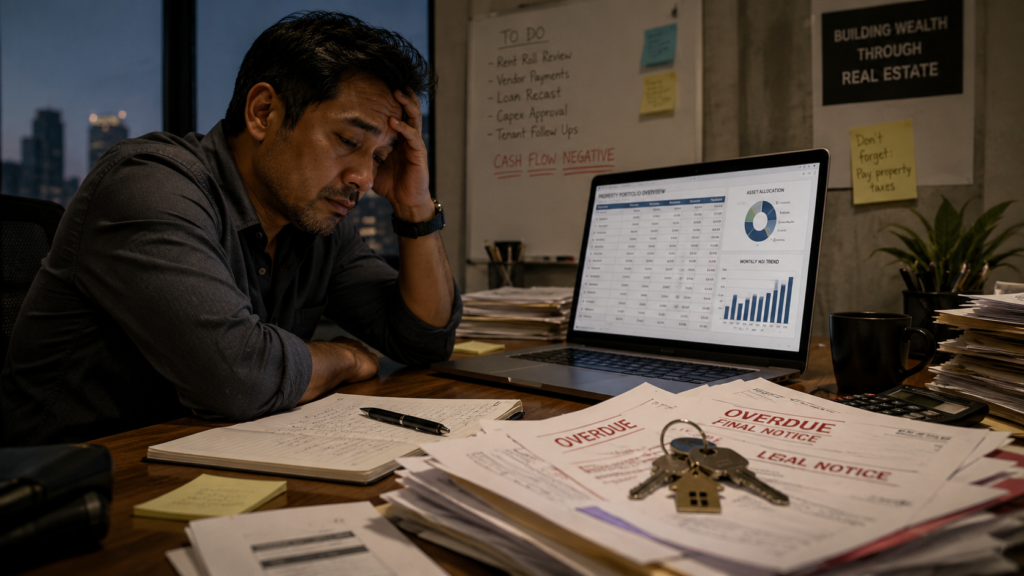

If you are currently losing sleep, watching interest compound, or facing aggressive demands from lenders over your buy-to-let mortgages within limited companies, you are not alone. The stress can make you physically ill, but hitting a wall with your portfolio doesn’t mean you are out of options. The key is understanding how corporate lending actually interacts with your personal life and how to build a professional strategy to protect what matters most.

At Bell & Company, we are debt strategists who protect people and their assets when property structures fail.

How Limited Company BTL Mortgages Create Personal Crisis

When times are good, a limited company buy-to-let mortgage works as expected. Your company owns the property and is responsible for the mortgage.

However, if your property business gets into financial trouble, lenders often look beyond the company structure.

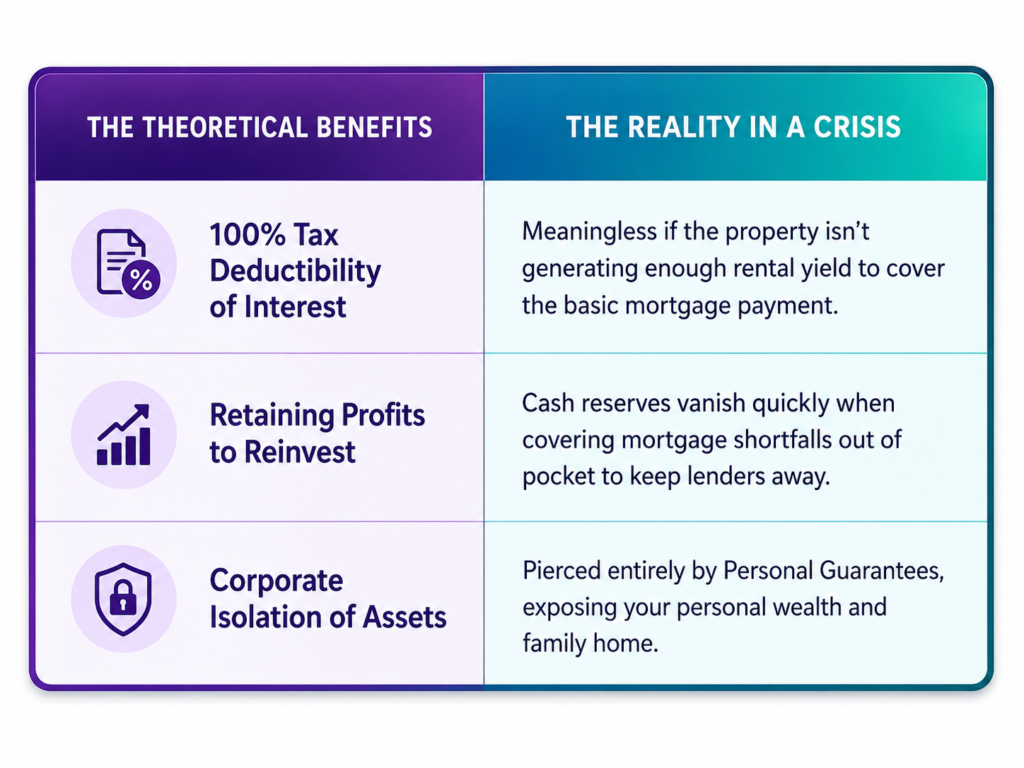

The Trap: Personal Guarantees

Most property SPVs (Special Purpose Vehicles: companies created solely to own and manage investment properties) don’t have years of trading history, therefore commercial lenders almost universally require a Personal Guarantee (PG) from the directors or major shareholders.

If you signed a PG, the limited liability protection of your company is effectively bypassed. The operational reality of a personal guarantee includes:

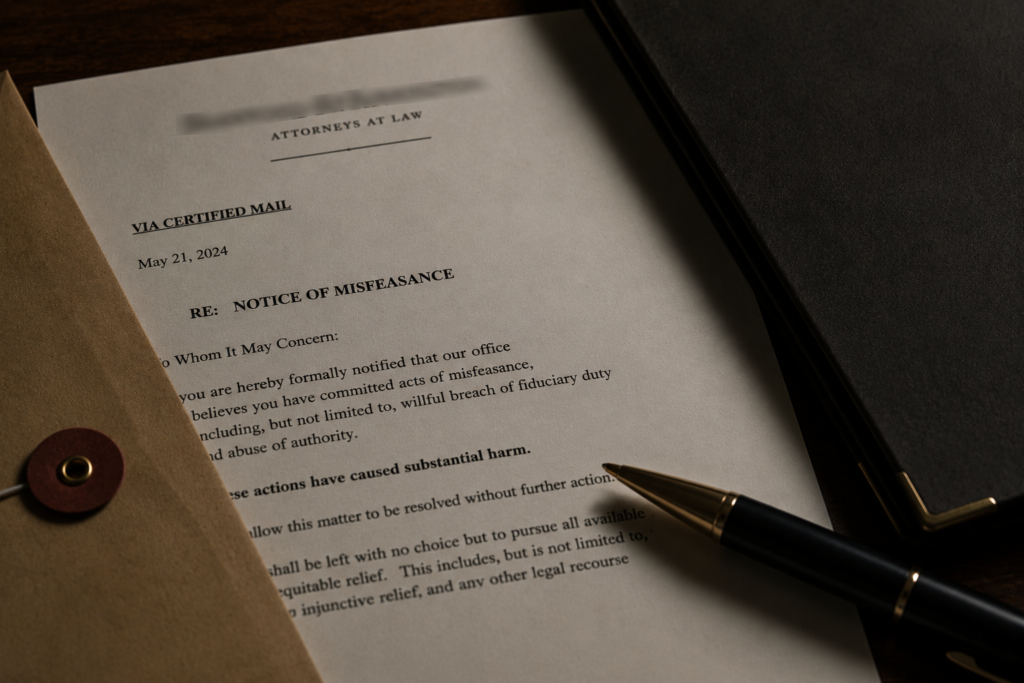

Ultimate Personal Liability: If the company falls behind on payments or faces repossession, the lender has the legal right to chase you personally for the shortfall.

Assets at Risk: This means your personal bank accounts, your investments, and, crucially, your family home can be targeted by lenders looking to settle the corporate debt.

Aggressive Pursuit: Specialist property and peer-to-peer lenders can be incredibly aggressive. Depending on the circumstances, they may appoint Law of Property Act (LPA) Receivers to take control of a rental property and collect rent on their behalf, begin possession proceedings, or use home visits and persistent contact to pressure directors into responding.

Threat of Bankruptcy: Creditors can, and often do, use Statutory Demands and the threat of personal Bankruptcy as a means to recover costs. It is also important to note that these costs don’t only include the shortfall. Many lenders also add default interest, legal fees, estate agent costs, marketing costs and the fees of any LPA Receiver appointed to manage or sell the property. These costs can substantially increase the amount ultimately claimed against you under a Personal Guarantee.

If you are in a position where you can’t afford your buy-to-let mortgage, you are no longer dealing with a simple corporate spreadsheet problem. The crisis is deeply personal and treating it like standard business administration can put your entire financial future at risk.

The Pressure Points of 2026 Criteria & Refinancing

Navigating the lending market in 2026 is exceptionally difficult for a landlord under pressure. If your current mortgage deal is coming to an end, or you are trying to refinance to find breathing room, you will face stringent criteria that can quickly compound your stress.

The Friction of High Product Fees

To make buy-to-let mortgages for limited companies’ rates look attractive on paper, the lending market has shifted heavily toward massive, percentage-based arrangement fees (frequently 2% to 5% of the loan amount).

While lenders do this to lower the headline interest rate and help properties pass the Interest Cover Ratio (ICR) rental stress tests, it creates an immediate barrier for cash-strapped landlords. If your portfolio is already struggling for liquidity, finding or adding thousands of pounds in corporate fees just to roll over a debt can push an over-leveraged business over the edge.

Strict Underwriting in Times of Distress

If the business is already faltering, it can be incredibly difficult to get a buy-to-let through a limited company. Mainstream providers require clean credit profiling of all major directors, strict maximum age limits, and often a minimum independent personal income of £25,000.

If a market downturn or regulatory backlog has hit your revenue, your corporate structure can quickly become a trap. Lenders are trained negotiators who know when you are cornered, and trying to handle complex refinancing or shortfall negotiations entirely on your own can leave you feeling like you are talking to a brick wall.

Weighing the Corporate Structure When It Starts to Fail

When a portfolio is thriving, the advantages of an SPV are heavily discussed. But when debts mount, you have to weigh the corporate friction points realistically.

The Realities of Corporate Property Distress

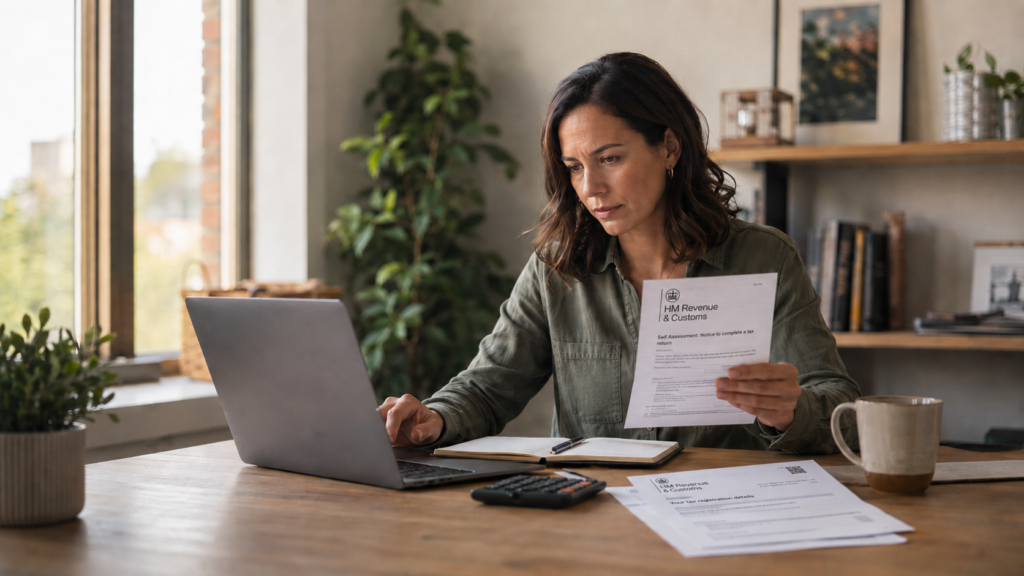

Furthermore, the accounting and administrative overhead required to maintain filings with Companies House and manage corporate tax returns doesn’t pause just because you are facing financial hardship.

Why Traditional Professional Advice Often Fails Landlords

When landlords realise they cannot sustain their corporate mortgage debt, they naturally turn to their traditional professional network. Unfortunately, these professionals are rarely equipped to protect a director’s personal life.

Accountants: They are experts at managing your books and tax returns, but they are not trained to negotiate with aggressive commercial lenders or manage high-stakes personal guarantee disputes.

Insolvency Practitioners (IPs): One of the most important distinctions to be aware of is what happens in the event of formal liquidation or administration. An Insolvency Practitioner operates under a statutory duty to act in the interests of creditors, not directors. While they deal with the company’s assets, creditors remain free to enforce any Personal Guarantees signed by directors separately.

Our Position: Wishing for the best outcome isn’t a plan. Lenders are experienced, well-resourced, and focused on their own position, which is exactly why having an independent strategist on your side isn’t a luxury; it’s a necessity.

Securing a Way Forward with Bell & Company

If your limited company property venture has become unsustainable, there is no benefit to delaying. Interest compounds daily and letting the situation spiral only worsens the toll on your health and family.

At Bell & Company, we are independent debt strategists. We do not follow a generic, one-size-fits-all insolvency process that sacrifices your personal wealth to satisfy commercial lenders. We act as a professional shield, taking over all creditor communication.

We forensically review your financial position, your documentation, and your net worth to establish realistic fallback strategies. Our track record speaks for itself: we routinely negotiate debt and personal guarantee reductions, protecting family homes, saving individuals from personal bankruptcy, and giving directors a genuine fresh start.

Contact Bell & Company today for a free, comprehensive case assessment with our senior consultants. Let us take the hassle and stress out of your hands so you can finally breathe again.

Get a Free Consultation Today

Worried about debt? We know that sometimes taking the first step can be the most difficult part.

Our experienced experts are always available to discuss your situation and provide options.

Contact us today for a free case review with one of our specialists.

Struggling with a Limited Company BTL Mortgage? 2026 Criteria, Personal Guarantees & Your Assets

Purchasing property through a corporate structure promised asset protection, but personal guarantees change the game. Discover how to shield your personal wealth when limited company buy-to-let mortgages face a financial crisis.

What is Misfeasance? A Director’s Guide to UK Corporate Insolvency Law

A misfeasance claim can expose directors to serious personal liability when a company enters insolvency. Find out what it means, how it differs from malfeasance, and what your options are.

Finance Act 2026: What Every Accountant and Tax Adviser Needs to Know About Mandatory Registration

HMRC's new mandatory registration regime directly tethers your right to practice to your firm’s internal tax compliance record. Discover how these changes might affect you.