If you are paid to manage another person’s tax affairs, the Finance Act 2026 has changed the ground beneath your practice. From 18 May 2026, HMRC began rolling out its mandatory registration regime for tax advisers, and the consequences of non-compliance are not a distant administrative headache. They are an immediate threat to your ability to work.

For most accountants, bookkeepers, payroll bureaus, and tax specialists, this is not a change you can quietly manage in the background. Your registration status is now directly tied to your firm’s own tax compliance record. This includes debts and overdue returns you may have been managing informally for years.

This briefing explains what has changed, where the risks sit, and what you need to do now.

Why Practice Debt Is No Longer Just a Cash-Flow Decision

Many practices have historically managed internal tax obligations – VAT, PAYE, Corporation Tax, personal Self Assessments – with a degree of pragmatic flexibility. Prioritising client commitments while running a rolling balance with HMRC was rarely comfortable, but it was manageable.

That underlying dynamics have now changed fundamentally.

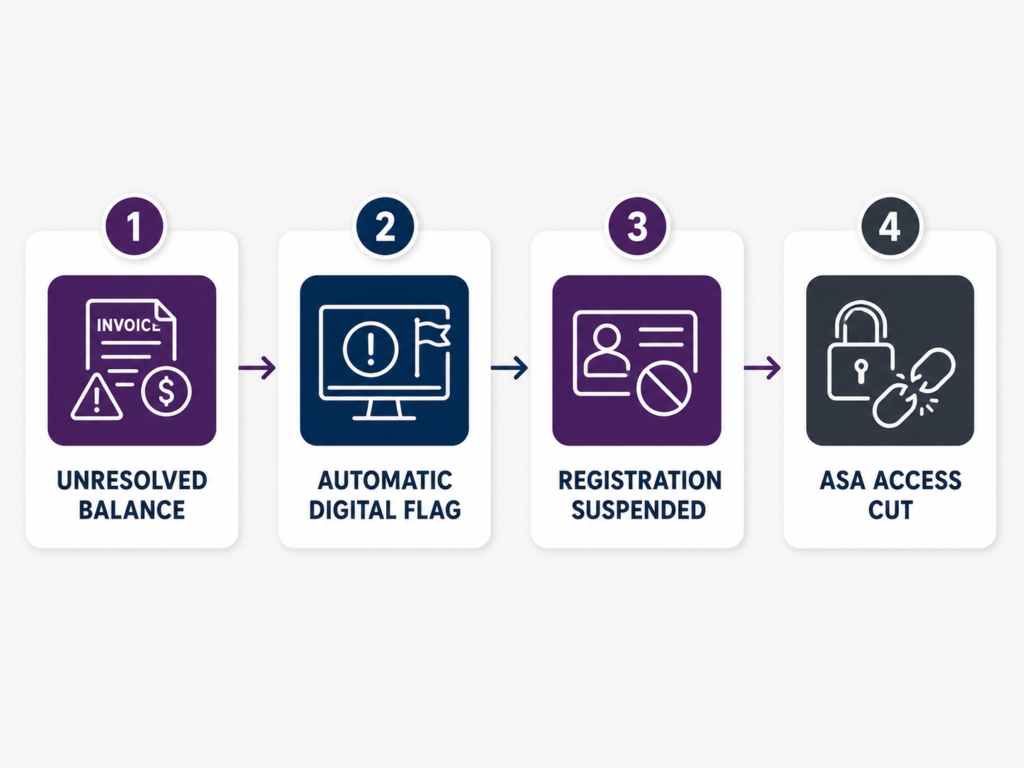

Under the Finance Act 2026 framework, outstanding internal liabilities are no longer a background risk. They are a direct trigger for registration blocks. And because the checks are automated, there is no discretionary review, no informal grace period, and no opportunity to explain your circumstances before access is cut.

This is the point that trips up most practices: having spoken to HMRC about a payment plan is not the same as having one.

Under the mandatory registration framework, a pending or unapproved Time to Pay (TTP) request does not satisfy the statutory requirements. Until HMRC has formally signed off a legally binding payment structure, the debt is classified as an unresolved liability.

That means it will trigger automatic registration blocks, regardless of any goodwill or informal assurances from a helpline. A formalised TTP arrangement, on the other hand, does satisfy the requirements – and protects your registration status while you work through the debt.

What Happens If Your Registration Is Blocked or Suspended

If your practice fails to register within its designated window, or has an active registration suspended due to flagged liabilities, the operational consequences are immediate:

- Practice Viability Risk: The rapid erosion of fee income, client retention, and cash flow that follows. A manageable tax liability can become an existential practice issue faster than most principals anticipate.

- Loss of Agent Services Account (ASA) Access: Your digital gateway to HMRC is blocked. Your team cannot submit VAT returns via Making Tax Digital (MTD), process payroll runs, or access client coding notices.

- Mandatory Client Notification: Under the Act, if your registration is suspended, you are legally required to notify your client base. Failure to do so carries an automatic statutory penalty of £5,000, rising to £10,000 for continued unauthorised interaction, alongside severe and irreversible reputational damage.

- Statutory Penalties: Continuing to represent clients or interact with HMRC while unregistered or suspended carries significant personal and corporate financial penalties.

The Clear Path Forward: What Practices Should Do Now

The framework does include a workable route for practices carrying liabilities, but it requires proactive, structured action. Waiting to see what happens, or relying on informal contact with HMRC, is the highest-risk approach available to you.

Treat your own compliance with the same rigour you apply to your clients:

- Conduct a thorough internal audit: Review all historic and current liabilities (VAT, PAYE, Corporation Tax, and personal Self-Assessments) across the practice entity and all key individuals.

- Clear outstanding compliance filings: Bring any overdue or late returns fully up to date. Registration cannot proceed if the underlying liability calculations remain unknown.

- Confirm your registration window: Identify the exact phase date assigned to your professional demographic and work back from your hard deadline.

- Formalise any payment arrangements: Convert any informal payment delays into a contractually binding Time to Pay arrangement well ahead of your registration window. Do not rely on a pending request or a verbal understanding.

Advisers Need Advisers Too

The Finance Act 2026 has created a new enforcement reality. For practices already navigating difficult economic conditions, an unresolved HMRC liability is no longer a deferred problem – it is directly tied to your right to practice.

We work with accountants, tax specialists, and practice directors facing exactly this situation – managing complex HMRC debts, personal guarantees, and practice liabilities under real commercial pressure. We handle all HMRC communications directly, negotiate structured Time to Pay arrangements, and work to protect your Agent Services Account status while you focus on your clients.

If you have concerns about how existing liabilities may affect your upcoming registration window, contact our team for a confidential conversation. The earlier we understand your position, the more options we have.