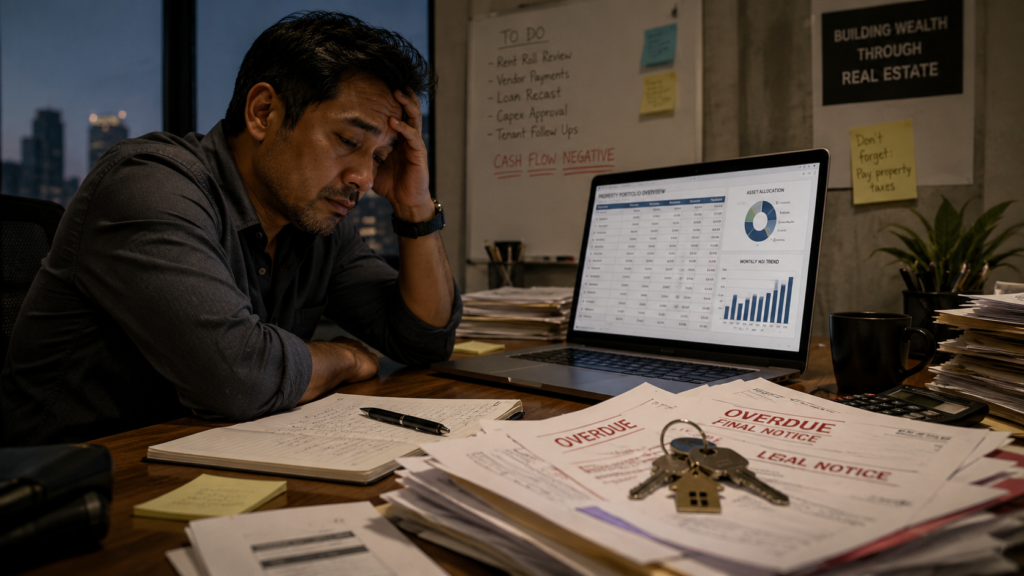

When your company enters insolvency, a letter from a liquidator alleging misfeasance can feel devastating. You may have spent years building the business, personally guaranteed loans, gone without a salary to keep staff paid, and now someone is telling you that you personally owe tens or hundreds of thousands of pounds.

That fear is understandable. But an allegation is not a judgment. Knowing exactly what you are facing is the first step to protecting yourself and safeguarding the things that matter most.

Defining Misfeasance: What Does It Mean in Law?

At its core, misfeasance means the improper, negligent, or flawed execution of an otherwise lawful act. In a corporate context, director misfeasance occurs when you perform your legitimate duties as a director, but do so with a level of negligence or breach of duty that harms the company, its shareholders, or its creditors.

The key word is negligence, not fraud. You do not need to have acted dishonestly for a misfeasance claim to arise. A poorly executed decision, such as selling an asset without a professional valuation or withdrawing funds the company could not afford, can be enough.

When your company enters financial distress, your duties under the Companies Act 2006 shift fundamentally. Your primary obligation is no longer to maximise shareholder returns. It becomes about protecting the interests of creditors. Decisions made after that point are examined through that lens, and any breach of duty can form the basis of a claim.

Misfeasance vs Malfeasance vs Nonfeasance: What Is the Difference?

These three terms are frequently confused. Understanding the distinction is important for assessing your own position accurately.

- Misfeasance means performing a lawful duty poorly, carelessly, or without due care.

- Example: transferring company assets to a new business without obtaining an independent valuation. You had the right to sell; you simply executed it negligently.

- Malfeasance means committing an inherently illegal or intentionally wrongful act.

- Example: directly defrauding the company, stealing cash, or deliberately fabricating records. This is intentional wrongdoing, not negligence.

- Nonfeasance means a complete failure to act when a legal duty explicitly requires action.

- Example: wholly abandoning your statutory responsibilities, ignoring critical safety obligations, or never filing accounts.

The distinction between misfeasance and malfeasance rests on intent and legality: misfeasance is a lawful act performed wrongfully; malfeasance is an act that is unlawful from the outset. Standard director misfeasance is a civil matter – a financial claim against you – not an automatic criminal offence. The criminal threshold is reserved for deliberate fraud.

Read our case study to see how we supported a client facing a misfeasance claim.

Director Misfeasance in Corporate Insolvency

In UK insolvency law, misfeasance claims are brought under Section 212 of the Insolvency Act 1986. This provides a summary mechanism that allows the court to bypass lengthy civil litigation and examine your conduct as a director directly. If a breach is established, the court can compel you personally to repay, restore, or account for misapplied company money or property, plus interest.

Under sections 170-177 of the Companies Act 2006, directors owe statutory duties that a liquidator will scrutinise: to act within powers, promote the company’s success, exercise independent judgment, apply reasonable skill and care, avoid conflicts of interest, and not declare unlawful dividends. Any breach, particularly once the company was approaching insolvency, can trigger a claim.

Who Can Bring a Misfeasance Claim?

While claims are most commonly initiated by an appointed liquidator or administrator, the law permits others to act where the company’s collapse has left significant unpaid debts:

- A liquidator or administrator is the most common route, driven by a commercial motive to recover funds for creditors.

- The Official Receiver is appointed by the court in compulsory winding-up proceedings.

- In specific circumstances, a creditor can seek court permission to bring a misfeasance claim independently if they believe the liquidator has failed to act on a clear breach of duty.

Real-World Examples: What Is an Example of Misfeasance?

Liquidators focus on specific operational decisions, not abstract legal theories. The following are the scenarios that most commonly give rise to claims.

Unlawful Dividends and Overdrawn Director’s Loan Accounts

Many SME directors take regular drawings throughout the year, intending to reclassify them as dividends at year-end. This is only lawful if the company has sufficient distributable reserves at the time the dividend is declared. If the company was loss-making or already insolvent, those drawings cannot become dividends. Rather, they remain an overdrawn director’s loan account, and the liquidator will demand personal repayment in full. This is one of the most frequent complaints made against directors, and one that routinely catches people off guard.

Preferential Payments

If you repaid a specific creditor ahead of others when insolvency was looming, particularly a loan you had personally guaranteed, while leaving HMRC’s VAT or PAYE arrears unpaid, a liquidator will treat this as a preferential payment. You are seen as having prioritised your own financial exposure over the wider creditor body. Liquidators can look back several years, so these transactions are rarely missed.

Transactions at an Undervalue

Transferring company assets, such as vehicles, equipment, intellectual property, and customer contracts, to a connected party or newly formed business at below market value is a serious red flag. Without an independent certified valuation and documented payment at full market value, the liquidator will treat this as a deliberate attempt to shield assets from creditors and seek to reverse the transaction or claim the shortfall from you personally.

Excessive Salary

Drawing a salary the company could not sustain while heading toward insolvency can also constitute misfeasance, as it reduces the funds available to creditors.

Legal Consequences: Liabilities, Limitation Periods, and Damages

A successful misfeasance claim can result in:

- Personal financial liability: the court may order you to repay misapplied or misappropriated company funds, compensate the company for losses caused by your conduct, or restore company property. Unlike many commercial claims, the focus is often on putting the company back in the position it would have been in had the misconduct not occurred. Courts frequently award interest on the sums due, which can substantially increase the amount payable, particularly where the conduct occurred several years before proceedings are issued.

- Director disqualification: findings of misconduct can lead to proceedings under the Company Directors Disqualification Act 1986. A disqualification order can prevent an individual from acting as a director, being involved in the promotion, formation, or management of a company, or instructing others how to manage a company, for a period of up to 15 years. Disqualification proceedings are civil rather than criminal and are brought relatively frequently by the Insolvency Service where director conduct is considered unfit.

- Legal costs: if the matter proceeds to court, the unsuccessful party will often be ordered to pay a substantial proportion of the successful party’s legal costs, in addition to their own. Given the complexity of insolvency litigation, costs can be significant and may exceed the amount originally in dispute.

- Claims brought years later: directors are often surprised to learn that liability can arise long after they have left office. A liquidator, administrator, or other officeholder may investigate historical transactions and commence proceedings after reviewing the company’s books and records. Depending on the nature of the claim and the circumstances, limitation periods may allow actions to be brought many years after the alleged misconduct occurred, particularly where concealment or fraud is alleged.

- Reputational and professional consequences: even where a claim settles before trial, allegations of misfeasance can damage professional reputation, affect future appointments, and create difficulties in obtaining financing, investment, or positions involving fiduciary responsibility.

The combination of personal liability, potential disqualification, legal costs exposure, and reputational damage means that misfeasance claims should be treated as a serious risk by any director, particularly when a company is experiencing financial distress or approaching insolvency.

Defending a Misfeasance Claim: How Bell & Company Protects Directors

Receiving an allegation of misfeasance is not the same as losing. It is an adversarial opening position, and there are well-established legal and commercial strategies to challenge, reduce, or resolve it.

Section 1157 – Statutory Relief

Under Section 1157 of the Companies Act 2006, a court has the discretionary power to relieve a director from personal liability, wholly or in part, where you can demonstrate that you acted honestly and reasonably and that, given all the circumstances, you ought fairly to be excused. Courts weigh factors including whether you personally benefited, the degree of harm to creditors, whether you acted on professional advice, and proportionality. Acting on what you genuinely believed to be sound guidance from an accountant or solicitor is a strong foundation for this defence.

Offsetting and Reduction

The amount claimed is not always as clear-cut as the first letter may suggest. In some cases, a director’s personal contributions to the business may be relevant when assessing the overall position. For example, money put into the company, payments made on its behalf, or other financial sacrifices made to support the business can help provide a fuller picture of the circumstances. A careful review of the facts is often needed before the true value of any claim can be determined.

The Commercial Reality

At Bell & Company, we do far more than simply respond to claims. From the moment you instruct us, we become the barrier between you and the liquidator, taking control of all correspondence and ensuring your position is presented clearly, professionally, and in its proper commercial context.

We understand that insolvency claims are rarely as straightforward as they first appear. Directors are often confronted with alarming allegations and inflated demands that fail to reflect the full picture. Our team has extensive experience challenging those claims, identifying weaknesses in the evidence, and negotiating substantial reductions in the amounts sought. In many cases, we have resolved matters for a small fraction of the original claim, helping clients avoid unnecessary financial and personal hardship.

Our focus is always on achieving the best possible outcome for you. Whether that means defending the claim outright, negotiating a commercial settlement, protecting personal assets, safeguarding the family home, or avoiding bankruptcy, we are committed to finding the most effective route forward.

Don’t Face Misfeasance Alone

If you have received a letter from a liquidator, been contacted regarding a director’s loan account, or have concerns about decisions made before your company’s insolvency, early advice can make a significant difference. Do not assume the liquidator’s position is correct, and do not face the process alone.

Contact Bell & Company today for a confidential, no-obligation case review. We act solely in your interests, providing clear advice, robust representation, and a practical strategy designed to protect your future.