Falling behind on tax payments is one of the most stressful challenges an individual or business owner can face. When dealing with HMRC debt management, the pressure can quickly feel overwhelming as automated letters pile up, interest accumulates, and late-payment penalties compound the original sum owed. However, outstanding tax arrears do not have to mean the closure of your company. By taking proactive steps, calculating what you can realistically afford to pay, and understanding how the debt management HMRC process operates, you can regain control of your financial future.

At Bell & Company, we specialise in providing expert corporate and personal HMRC debt help. Whether your business is struggling with a single late payment or facing aggressive enforcement across multiple tax heads, this guide outlines the practical steps required to navigate the HMRC debt management team and secure a sustainable resolution.

Getting in Control of Tax Arrears

The most critical mistake any director or taxpayer can make is ignoring communications from HMRC. When a business falls into financial distress, the initial instinct may be to delay filing returns or hide from incoming mail. However, early intervention remains your strongest asset when seeking help with HMRC debt.

Before you speak with a tax collector, you must establish a clear financial baseline. This requires a meticulous review of your company’s cash flow, which includes:

- Calculating total income: Documenting all incoming revenue streams accurately.

- Assessing business outgoings: Identifying essential operational costs versus non-essential corporate expenses.

- Determining disposable income: Working out the exact surplus cash available to put toward a structured repayment plan.

Having a transparent, accurate understanding of these figures prevents you from agreeing to an unrealistic payment schedule that your business cannot maintain over the long term.

Managing Specific HMRC Tax Liabilities

Different types of tax debts carry distinct financial implications and require unique approaches when dealing with HMRC’s debt management team. Understanding how each tax impacts your company is vital to resolving your broader HMRC Business Debt.

VAT Debt Management

Value Added Tax is viewed strictly by HMRC because businesses act as custodians, collecting this tax from customers on behalf of the government. Consequently, HMRC is notoriously aggressive when dealing with VAT arrears. If your business is falling behind, establishing a strategy for dealing with your VAT debt quickly is essential to protect your day-to-day trade. Mismanaging HMRC VAT debt can quickly trigger severe penalties and enforcement visits by field staff.

Corporation Tax Debt Management

An outstanding corporate tax bill can stall growth and limit your access to traditional asset finance. Implementing an effective approach to HMRC corporation tax debt management ensures that temporary profitability issues do not result in forced insolvency or winding-up proceedings.

PAYE Debt Management

Pay As You Earn (PAYE) and National Insurance Contributions (NICs) are absolute priority debts. HMRC treats unpaid employee deductions with high severity. Staying on top of HMRC PAYE payments is non-negotiable if you want to avoid personal liability threats or direct enforcement actions against your company assets.

Self-Assessment Debt Management

For sole traders, partners, and directors with personal liabilities, navigating HMRC self-assessment demands immediate attention. Unlike limited company debts, self-assessment arrears put your personal assets, including your family home, directly at risk.

If your business is struggling across one or more of these fields, review our comprehensive hub on HMRC Business Arrears to understand your core rights and initial options.

Negotiating with the HMRC Debt Management Team

Can you negotiate with the revenue? Yes, you can. The primary mechanism for settling outstanding tax arrears over time is a Time to Pay (TTP) arrangement. A TTP arrangement is a formal agreement that allows a business or individual to clear their debt via monthly instalments, typically over a period of 6 to 12 months, though longer terms can be negotiated in specific circumstances.

Securing a TTP arrangement requires presenting a robust, evidence-backed proposal to the HMRC debt management helpline. However, navigating these negotiations has become increasingly difficult due to changing internal processes. As outlined in our article on the HMRC AI Attack, HMRC has increasingly turned to automated systems and AI algorithms to assess risk and manage collections. This shift means that proposals must be flawless and compliant with automated parameters to avoid immediate automated rejection.

Working with an experienced HMRC debt management company can drastically improve your chances of approval. For instance, our team successfully assisted a healthcare provider by securing a 36-Month Time to Pay Arrangement Secured With HMRC, providing them with the breathing room necessary to sustain operations. Similarly, you can read about Saving a Domiciliary Care Business to see how a structured, professionally presented cash-flow case study can convince HMRC to grant long-term relief.

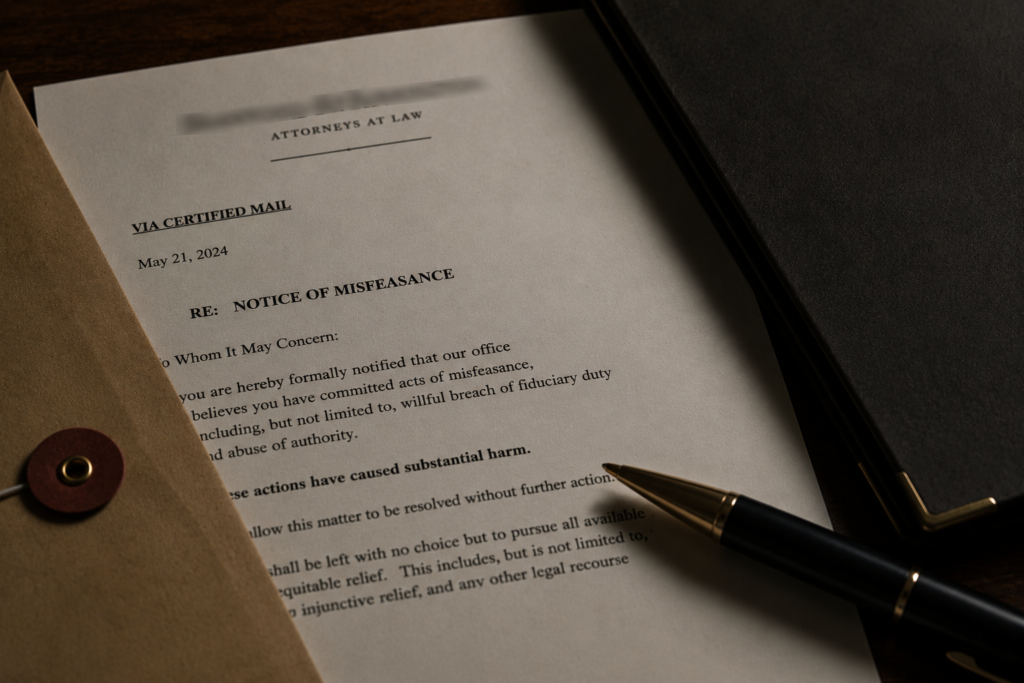

The Risks of Ignoring HMRC Enforcement

If communication breaks down or if you fail to engage entirely, HMRC will quickly escalate their collection tactics. They hold unique, sweeping legal powers that ordinary commercial creditors do not possess.

To understand the full gravity of non-payment, watch our informational videos detailing What Happens If You Ignore HMRC Debt Letters? and Can HMRC Close Down Your Company Due to Unpaid Taxes?.

If left unchecked, enforcement actions can include:

- Notice of Enforcement: A statutory prelude to taking control of goods and inventory.

- Direct Detriment to Bank Accounts: Directly seizing funds from your business or personal bank accounts.

- Winding Up Petitions: Forcing your limited company into compulsory liquidation.

If your business is being targeted by aggressive debt collectors, read our guide on how to handle Aggressive Creditors. If a petition has already been issued, immediate specialist legal action is required. Review our survival guide on having Received a Winding Up Petition from HMRC to see how closure can be prevented.

Even when facing severe legal threats, positive outcomes are possible. For example, our team successfully intervened to ensure a £72,000 HMRC Winding Up Petition was Avoided entirely for a client, protecting their brand and business continuity. For another owner, our support facilitated a journey From Fear to Freedom, proving that structured debt intervention can restore peace of mind.

Frequently Asked Questions About HMRC Debt Management

What is the 4 year rule for HMRC?

The 4-year rule refers to the standard statutory time limit for HMRC to issue an assessment for underpaid tax or correct an error on a past return. Under normal circumstances, HMRC cannot go back further than 4 years to claim unpaid taxes if the taxpayer made a careless but non-deliberate mistake.

How to clear HMRC debt?

To clear your tax debt, you must either pay the balance in full immediately or propose a formal payment schedule. The most effective method for operating businesses is negotiating a Time to Pay (TTP) arrangement, backed by clear evidence of affordability, cash-flow forecasts, and documented disposable income.

Can HMRC debt be written off?

HMRC will rarely write off debt voluntarily for an active individual or operating company. However, if a limited company is genuinely unviable and enters formal insolvency practices, the remaining unsecured tax debts can potentially be restructured or legally discharged.

Which debt collection agency does HMRC use?

HMRC utilises a select panel of private external debt collection agencies to recover outstanding arrears when taxpayers fail to respond to early warnings. Some of the agencies frequently appointed by HMRC include 1st Locate (trading as LCS), Westcot Credit Services, Advantis Credit, Ardent Credit Services (DRS), and Bluestone Consumer Finance.

How far back can HMRC go for unpaid tax?

The look-back period depends entirely on the nature of the tax discrepancy:

- 4 years for innocent, documented mistakes.

- 6 years for careless or negligent behaviour where reasonable care was not taken.

- 20 years if HMRC establishes that the taxpayer deliberately evaded taxes or engaged in fraudulent behaviour.

What happens if I can’t pay HMRC debt?

If you cannot afford to clear your balance, interest will accumulate daily alongside late payment penalties. If you fail to propose a formal payment resolution, HMRC will transition the file to enforcement, which may result in debt collection agency assignment, asset seizure, or a winding-up petition designed to shut your business down.

Can you negotiate with HMRC?

Yes. HMRC prefers to collect outstanding tax over an extended duration rather than forcing an operational business directly into compulsory liquidation, provided the business demonstrates honesty and transparency. Negotiation is entirely feasible if you present a realistic, well-supported Time to Pay proposal.

Is it true that after 7 years, your credit is clear?

While standard consumer credit defaults, County Court Judgments (CCJs), and bankruptcies are removed from UK credit files after 6 years from the date of issue, this rule does not mean tax debts disappear. If HMRC has an open, active assessment or ongoing judgment against you, the liability remains legally enforceable until paid or formally discharged through insolvency.

Act Now on Priority HMRC Debt

If your business is facing a tax crisis, procrastination will only reduce the options available to you. Contact Bell & Company today to receive dedicated, professional support in managing your tax liabilities and dealing effectively with the HMRC debt management team. Let us handle the pressure of the revenue so you can focus on running your business.