Facing a financial crisis within your limited company can feel like an isolating and even threatening experience for the director going through it. We often speak to directors who say they are “extremely worried”, physically ill from stress, or completely overwhelmed by a situation that feels like an absolute “kick in the teeth.” Financial pressure is never just a numbers game. It breaks through the boardroom wall, invading your home life, draining your health, and straining the relationships that matter most.

When creditors escalate their demands, receiving a winding-up petition is a serious flashpoint, but it does not mean you have run out of options. Hope is not a strategy. Early action is.

At Bell & Company, we are independent debt strategists, not Insolvency Practitioners (IPs). We work for you, not your creditors. While a liquidator’s statutory duty is to act in the interests of the company’s creditors, our sole focus is acting as your structural shield, protecting your home, your family, and your future from the fallout of compulsory liquidation.

What is Compulsory Liquidation?

Compulsory liquidation is a formal, court-ordered legal process where a limited company is forced to shut down permanently. It represents the ultimate breakdown in communication between an insolvent business and its creditors, resulting in a judge ordering that the company be wound up and its assets come under the control of a liquidator.

Why Would a Company Go into Compulsory Liquidation?

A company is forced into compulsory liquidation because it is legally insolvent, meaning it is unable to pay its bills when they fall due, or burdened with liabilities that outweigh its assets.

In the vast majority of cases, HMRC is the primary petitioner when you’re behind on VAT, PAYE, or Corporation Tax – and the data backs this up. In the six months to May 2026, HMRC issued 1,192 winding-up petitions, accounting for 64.9% of every petition filed in England and Wales during that period, equivalent to an average of 6.5 HMRC petitions every single working day. Clients who have appointed our services have said that ‘navigating HMRC’s bureaucracy can feel like talking to a brick wall’ when they try to resolve the issue themselves. If left unaddressed, HMRC or other frustrated trade creditors will issue a winding-up petition. The minimum debt required to liquidate a company via this court route is £750.

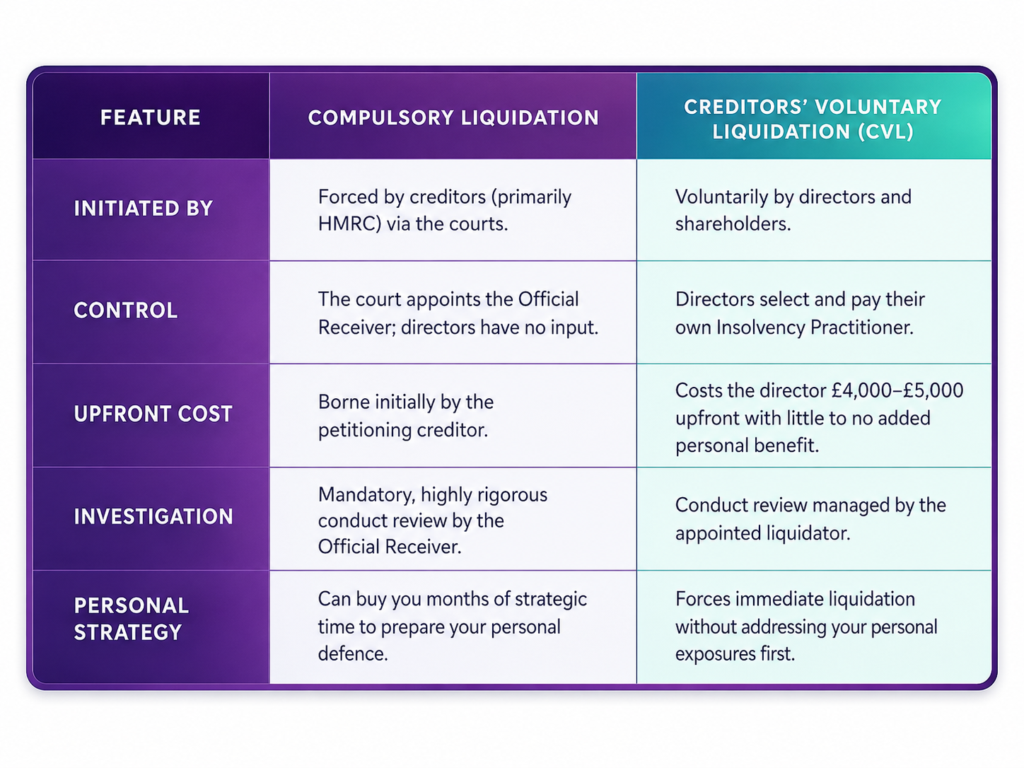

Compulsory Liquidation vs Creditors’ Voluntary Liquidation (CVL)

Directors are often desperate for alternatives to avoid liquidation entirely, or they lean toward a voluntary route because they want to maintain a sense of control. However, there are deep misconceptions about the differences between compulsory liquidation vs voluntary liquidation:

The Step-by-Step Compulsory Liquidation Process & Timeline

When you are under immense emotional strain, conflicting advice from accountants, IPs, and brokers only fuels the confusion. To cut through the noise, here is exactly what happens during the compulsory liquidation process in the UK:

1. The Winding-Up Petition (WUP)

The formal process begins when an unpaid creditor files a petition with the court. You do not need to attend court at this exact moment, but a strict legal countdown begins.

2. The Freezing of Bank Accounts

A major shock for most directors is when their business banking is suddenly cut off. Company bank accounts are typically frozen around 12 days before the public court hearing advertisement is published. Once frozen, the business cannot make payments, making it effectively impossible to continue trading.

3. The Court Hearing

The formal court hearing typically takes place 8 to 10 weeks after the petition is originally served. If the debt cannot be settled or an adjournment isn’t strategically negotiated, the judge grants a Winding-Up Order.

4. Appointment of the Official Receiver & Asset Realisation

Control is instantly stripped from you. The Official Receiver (OR) or an appointed liquidator steps in to sell company assets to pay off creditors. This process is slow, typically lasting 3 to 6 months (or longer), but it drastically accelerates creditor aggression against you personally.

What Does the Liquidation Process Involve for Directors?

Many company directors mistakenly believe that the “limited liability” structure of a limited company completely insulates them from the business’s debts. In a compulsory liquidation, this is a dangerous misconception. The process changes your role from a decision-maker running a business to a subject of an intense, mandatory government investigation. It involves handing over all books, records, and control, leaving you completely exposed to personal liabilities if your affairs are not strategically managed beforehand.

Can a Company Continue Trading in Compulsory Liquidation?

No. The moment a Winding-Up Order is granted by the court, the company must cease trading immediately. Your powers as a director are instantly revoked. You lose all access to company bank accounts, assets, and operations. Trying to continue trading past this point is illegal and will look incredibly damaging to the court and the liquidator.

Can a Director Be Held Personally Liable After Liquidation?

Yes, absolutely. This is the single biggest area of fear and confusion for directors under stress. Limited liability does not protect you from personal exposures like Personal Guarantees (PGs) or an Overdrawn Director’s Loan Account (DLA).

- Personal Guarantees: If you signed a PG for a business loan, overdraft, or commercial lease, those lenders (such as fintech lenders or traditional banks) are waiting in the wings. The moment the company enters liquidation, those PGs activate. Suddenly, a corporate debt becomes an immediate personal demand for tens or hundreds of thousands of pounds, putting your family home and personal vehicles at risk.

- See how our expert debt strategists successfully negotiated with aggressive lenders to save a used car dealer’s family home during a major UK trade insolvency crisis. Read the Full Case Study

- Overdrawn Director’s Loan Accounts: If you drew money from the business that wasn’t processed as legitimate salary or dividends, the liquidator will view this as a debt you owe back to the company. They will pursue you aggressively to repay every penny to satisfy corporate creditors.

- Discover how we stepped in to protect a director facing total personal exposure and the threat of personal bankruptcy after their corporate liquidation triggered aggressive creditor demands. Read the Full Case Study

Watch our video on how corporate liquidation activates personal liabilities and learn how to manage your exposure:

Watch: Business Liquidation & Personal Exposure Management

Director Disqualification and the Official Receiver’s Investigation

In every single compulsory liquidation, the Official Receiver is legally required to investigate your actions leading up to the insolvency. They are looking to realise money and will scrutinise your books for:

- Wrongful Trading: Continuing to trade and incur debt when you knew the company was insolvent.

- Preferences: Paying off certain creditors (like family members or connected businesses) ahead of others, such as HMRC.

- Illegal Dividends: Declaring dividends when the company did not have the profits to support them.

If the investigation uncovers unfit conduct, you can face severe consequences, including director disqualification for up to 15 years, personal liability for company debts, or even criminal charges in cases of fraud.

How Much Does a Compulsory Liquidation Cost?

Who Pays the Costs of Liquidation?

The initial administration and court fees of a winding-up petition are paid for by the creditor who issues it. Once the process begins, the costs are funded directly out of the realisation of the company’s remaining assets.

How Much Tax Do I Pay If I Liquidate My Company?

In an insolvent compulsory liquidation, because the company is forced to close by creditors, there are rarely cash distributions left over for shareholders. Therefore, personal Capital Gains Tax via Business Asset Disposal Relief is not applicable. Any outstanding corporate tax liabilities remain with the company, unless HMRC pursues a Personal Liability Notice against a director for deliberate neglect or fraud.

Outcomes: What Happens After Compulsory Liquidation?

Once the assets are sold and the investigations are complete, the company is formally dissolved and struck off the Companies House register.

Who Will Be Paid First in the Liquidation?

The proceeds from asset realisations are paid out in a strict hierarchy governed by UK insolvency law:

- Costs of the Liquidation: Realisation fees and Official Receiver costs.

- Secured Creditors (with a fixed charge): Typically, banks holding charges over property or land.

- Preferential Creditors: Employee wages and holiday pay, alongside HMRC as a secondary preferential creditor for taxes like VAT and PAYE.

- Secured Creditors (with a floating charge): Lenders with a charge over shifting assets like stock.

- Unsecured Creditors: Trade suppliers, contractors, and unsecured business loans.

- Shareholders: Only receive funds if all other debts are paid in full (extremely rare in compulsory liquidations).

What is the Downside of Liquidating a Company?

The downsides of allowing your company to fall into compulsory liquidation are stark if you enter the process unprotected:

- Total Loss of Control: The court takes over; you lose the ability to manage the narrative or guide the business wind-down.

- Severe Credit and Reputational Damage: Winding-up petitions are published publicly, destroying trade relationships and making it exceptionally difficult to secure financing for future ventures.

- High Risk of Personal Exposure: The mandatory investigation puts your personal wealth, loan accounts, and family home directly under the microscope of an aggressive government receiver.

Key Takeaways for Directors Facing Compulsory Liquidation

- A limited company structure is not an absolute shield. Personal guarantees and director’s loan accounts will follow you home after corporate failure.

- The Official Receiver works for your creditors, not you. You need independent representation to advocate for your personal interests.

Don’t Let Creditors Decide Your Future. Let’s Build a Strategy.

If you are currently sick with worry, facing an aggressive HMRC petition, or terrified of what an overdrawn loan account or personal guarantee will do to your family home, please know that you can breathe again.

We understand how deeply personal and physically exhausting this is. We provide a completely free, no-obligation forensic case assessment where we look closely at your documentation, unpack the exact breakdowns of what you owe, and map out a clear, step-by-step strategy.

Once you instruct us, we take over all creditor correspondence immediately. This means you will never have to speak to an aggressive debt collector, HMRC, or lender again.al and independent strategy review. Let us sit on your side of the table and protect what you have worked so hard to build.

Take Back Control of Your Life Today

Call our senior consulting team now or click below to secure your free case review. Let’s stop the panic, block out the noise, and build the defence strategy you need for a genuine fresh start.

Bell & Company – Expert, independent debt strategists standing firmly in your corner.