If your company is facing severe financial pressure, you are likely feeling completely in the dark about what the next week or month will bring. Between mounting HMRC business arrears, threat letters, and the constant fear of personal assets such as your family home being caught in the crossfire, the stress can feel entirely overwhelming.

When a business enters severe distress, two corporate terms are frequently thrown around: administration and receivership.

Many directors assume these processes are identical, or they mistake them for basic business liquidation. They are not. Entering either route without a clear strategy can trigger personal consequences – from personal guarantee exposure to aggressive director loan account investigations.

This guide breaks down the critical differences between administration and receivership in plain English, highlighting the hidden risks to your personal assets and detailing how to regain control of your commercial future.

Is an Administrator the Same as a Receiver?

Yes and no. While an administrator and a receiver play very different roles within formal insolvency events, in both cases, it is an insolvency practitioner (IP).

When clients call our team, a major point of confusion is practitioner loyalty. Many directors mistakenly believe that the licensed insolvency practitioner walking through their door is there to save them or protect their interests.

As we routinely advise during our client strategy consultations, the receiver or administrator, unfortunately, isn’t there for you. They are there for the creditors. However, how they serve those creditors differs fundamentally.

The Role of an Administrator

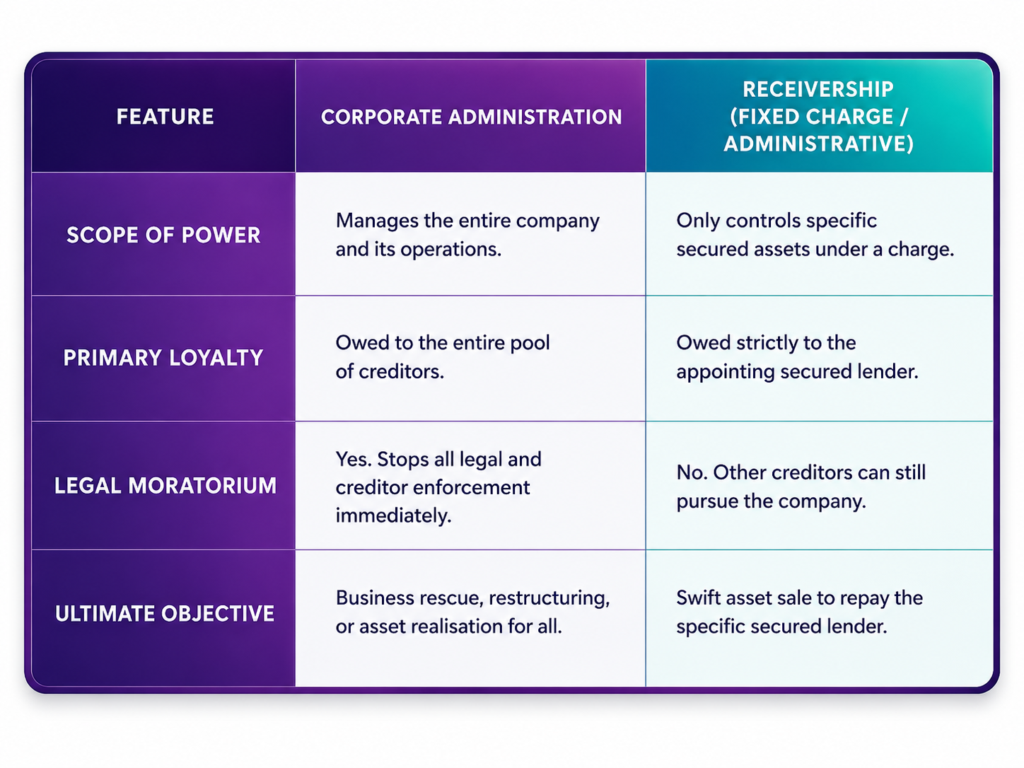

An administrator is appointed to take over management of the whole company. Their legal mandate is to attempt to rescue the company as a going concern, achieve a better result for creditors than an immediate liquidation would, or realise property or other assets to make a distribution to secured or preferential creditors.

- Who they act for: They owe a statutory duty to all creditors as a collective whole, not just one lender.

- The key benefit: The moment a company enters administration, an automatic legal moratorium is placed around the business. This acts as a legal shield, halting any active debt collection, statutory demands, CCJs, or winding-up petitions.

The Role of a Receiver

A receiver – most commonly an Administrative Receiver or a Fixed Charge Receiver – is appointed by a secured lender (such as a bank) holding a specific charge over company assets.

- Who they act for: Unlike an administrator, a receiver owes their primary allegiance to the appointing lender. Their sole objective is to take possession of the pledged assets, manage them, collect income, and oversee their sale to claw back money for that specific bank or creditor.

- The key downside: Receivership does not provide an automatic, company-wide legal moratorium to protect the wider business from other hostile creditors.

Why Would a UK Company Go Into Receivership or Administration?

Both procedures indicate severe underlying financial distress, but they are triggered by entirely different commercial mechanics.

Triggers for Corporate Administration

A company typically enters administration when it is facing acute cash flow insolvency or balance sheet insolvency, yet the core business remains viable. It is often used as a defensive mechanism.

Directors might opt for this route when they realise that business debt pressures have become completely unmanageable, or when a major creditor threatens to force the business into compulsory liquidation.

Why a Company Faces Receivership

Receivership is rarely a choice made by the directors; it is an aggressive enforcement action taken by a lender.

It is triggered when a borrower defaults on a loan agreement. This usually follows a pattern of missed property or asset repayments, failed formal payment arrangements, or a complete breakdown in creditor communication. If the bank loses confidence in your ability to repay, they exercise their contractual right under their debenture or legal charge to appoint a receiver to seize control of the asset.

What Happens if a Company is in Receivership or Administration?

The reality of entering either process can feel chaotic, fast-paced, and highly unfair. Many clients we speak with express deep frustration that multiple parties are suddenly involved, and nobody seems to communicate transparently.

In Administration: The powers of the company directors are completely suspended. The administrator steps into your shoes, takes over all operations, and has the authority to make staff redundant, terminate contracts, or sell parts of the business. They will assess whether the company can be saved via a Company Voluntary Arrangement (CVA), sold as a going concern, or wound down into liquidation.

In Receivership: The receiver takes physical and legal possession of specific, or in some cases all, assets covered by the lender’s security (such as commercial property, land, or specialised machinery). They have vast powers to manage or operate these assets, collect any rental income, and aggressively push for a sale.

While you may technically retain control over the rest of the company, losing your core operational assets often renders the wider business impossible to run. Furthermore, banks can sometimes act incredibly fast; we have supported clients where lenders “acted a bit sneaky,” giving minimal notice before appointing a receiver.

What Are the Three Types of Administration Routes?

If administration is pursued, the insolvency framework provides three distinct procedural routes to appoint an administrator:

1. Court Route

This involves a formal court hearing. It is typically utilised when creditors, or the directors themselves, apply via the court system because the company’s legal situation is highly complex, or because a winding-up petition is already active against the business.

2. Out-of-Court Route (Directors/Company)

This is a faster, more streamlined choice made directly by the company’s board of directors or shareholders when insolvency is imminent. By filing specific notices at court, the board can rapidly install an administrator of their choosing to gain immediate breathing space and protect the business from pending creditor action.

3. Out-of-Court Route (Qualifying Floating Charge Holder – QFCH)

This route is triggered by a creditor holding a qualifying floating charge over the whole or substantially the whole of the company’s assets. This can include banks, alternative lenders, bond trustees, or any creditor whose security instrument creates a floating charge over largely all of the company’s property. Once a default or other trigger event occurs, the QFCH can appoint an administrator of their choice by filing prescribed forms at court, without requiring a court hearing or judicial approval. Before doing so, notice must be given to any prior-ranking QFCH, who has a short window to appoint their own administrator first.

Who Gets Paid First in Administration?

When an administrator sells company assets, the distribution of funds follows a rigid statutory hierarchy set out by UK insolvency law.

A common complaint from directors experiencing this process is that insolvency practitioners seem “quite happy to rack up massive costs,” often walking away with a significant portion of the money while ordinary creditors receive pennies. This occurs because fees are positioned at the very top of the legal payment waterfall:

- Secured Creditors with a Fixed Charge: Paid directly from the sale of the specific assets secured by the charge (e.g., property).

- Insolvency Practitioner Fees & Expenses: The costs and high hourly rates incurred by the administrator during the process.

- Preferential Creditors: This includes employee wages, holiday pay, and crucially, HMRC for certain taxes like VAT and PAYE.

- Secured Creditors with a Floating Charge: Lenders with a charge over shifting assets (e.g., stock or debtors).

- Unsecured Creditors: Trade suppliers, contractors, and utility providers. They are at the bottom of the ladder and rarely receive full repayment.

- Shareholders/Directors: Only paid if a surplus remains, which is exceptionally rare in formal insolvency.

Why Waiting for an Insolvency Practitioner Is a Bad Idea

If you believe that putting your business into administration or waiting for a bank to appoint a receiver will magically wipe your hands clean of corporate debt, you are facing a severe risk.

Most debt does not stay on a balance sheet. It follows you home.

Many directors assume administration is the default or only way to rescue a business, but in a lot of cases, there are other, more suitable alternatives. Contact Bell & Company to find out your options. Relying solely on a formal insolvency practitioner poses massive personal risks:

- Personal Guarantees Will Be Triggered: The moment your business enters formal administration or receivership, your banks, secondary lenders, or landlords will immediately call in your personal guarantees. An insolvency practitioner cannot help you negotiate your personal guarantees – doing so would represent a massive conflict of interest with their statutory duties to creditors.

- Director Loan Account Scrutiny: Administrators are legally mandated to investigate director conduct. If you have an overdrawn Director’s Loan Account (ODLA), the administrator will aggressively pursue you personally to repay that cash back into the corporate pot.

- Asset Exposure: If personal guarantees are triggered and you cannot immediately raise the funds, your personal assets – including your family home – are placed at immediate risk of charging orders, statutory demands, and personal bankruptcy.

Consider this real-world case study: A UK director faced corporate collapse when business debt turned into severe personal liability. Watch this video breakdown detailing how business debt routinely becomes personal to understand exactly what occurs behind closed doors.

How Bell & Company Helps Directors Navigate Administration and Receivership

We want to be entirely clear: Bell & Company are not insolvency practitioners, liquidators, lawyers, or accountants. While our multi-disciplinary team is comprised of experts from those exact backgrounds, we operate strictly as an independent debt strategy firm.

We do not work for your banks, your lenders, or your creditors. We work exclusively for you, the director.

An insolvency practitioner’s job is to harvest assets for the creditors. Our job is to act as your structural shield, protecting your livelihood, your family home, and your personal financial future.

Our Strategic Approach

We do not believe in off-the-shelf formulas or rushing into destructive, expensive formal procedures. We look at the macro picture to build a bespoke debt strategy around your personal priorities.

- Pre-Insolvency Negotiation: We evaluate whether you can bypass formal insolvency entirely by opting for non-formal debt solutions or strategic pre-insolvency negotiations.

- Personal Guarantee & ODLA Defence: If administration or receivership is completely unavoidable, we step in to negotiate, reduce, and settle your personal guarantee liabilities and overdrawn director loan accounts directly with lenders.

We have over a decade of experience and have saved over £400 million for our clients. Our corporate debt strategies are built entirely on proven, real-world outcomes, not theories.

Take a look at how we provided comprehensive bankruptcy and asset protection support to a client facing £150,000 of aggressive debt, and watch our asset protection success story video to see how strategic intervention saves homes.

Act Before Decisions Are Made for You

In the current economic climate, many corporate teams are struggling with the growth vs. reality paradox, facing insolvency despite underlying commercial potential.

Hope is not a strategy. If your company is facing the threat of administration or asset receivership, early intervention is the only way to retain control.

Contact Bell & Company today on 0333 305 4331 or fill out our contact form for a confidential and independent strategy review. Let us sit on your side of the table and protect what you have worked so hard to build.