If you are a director facing Personal Guarantee exposure, the question of “bankruptcy or IVA?” is rarely just a personal debt decision.

It is a question about; protecting your home, protecting your income, protecting your family’s financial position, and understanding how to deal with creditor pressure before the situation escalates further

By the time many directors begin considering these options, the pressure has already become significant.

You may already be dealing with; demands from creditors, HMRC arrears, legal threats, failed payment arrangements, or concerns about how business borrowing could affect you personally.

And often, the advice can feel contradictory.

One adviser may tell you that an Individual Voluntary Arrangement (IVA) is the safest route because it avoids bankruptcy. Another may suggest bankruptcy would be faster, cleaner, or more realistic financially. Your accountant may be focused on preserving your directorship. Meanwhile, creditors may already be threatening enforcement action.

Online, you will also find a huge amount of generic debt advice, much of which does not properly consider the additional complexities that arise when Personal Guarantees, business liabilities, and home equity are involved.

The reality is that there is no universal answer.

For directors with Personal Guarantee exposure, the right solution depends entirely on the wider commercial picture, not simply which insolvency procedure sounds less severe.

The real question is not simply:

Is bankruptcy or an IVA better?

The better question is:

Which route gives you the strongest outcome once your personal guarantees, income, home, creditors, job role and long-term plans are properly assessed?

That is what this guide explains.

Why You’re Getting Conflicting Advice?

Directors often receive conflicting advice because different professionals view the same situation through different lenses.

An Insolvency Practitioner may recommend an IVA. A debt charity may lean towards bankruptcy. An accountant may focus on protecting your directorship. Meanwhile, creditors may push whichever route gives them the strongest recovery position.

That does not necessarily make the advice wrong.

But it can mean the advice is incomplete.

For many directors, the situation involves far more than straightforward personal debt. It may include:

- Personal Guarantees

- Business loans

- HMRC arrears

- Overdrawn Director’s Loan Accounts

- Trade creditors

- Asset finance liabilities

- Home equity

- Personal borrowing used to support the business

This is why generic advice can be misleading.

An IVA proposal may not fully address Personal Guarantee exposure. Bankruptcy risks may be overstated. The long-term affordability of repayment plans may not be properly tested.

At Bell & Company, many clients tell us they felt more confused after speaking to multiple advisers than they did at the start. Often, they had not been shown:

- The true cost comparison between options

- What happens if an IVA fails

- Or how trustee negotiation can influence bankruptcy outcomes

This is the gap we aim to close.

Bankruptcy or Individual Voluntary Arrangement (IVA): The Facts

Before asking what is better, IVA or bankruptcy, you need to understand what each route actually does.

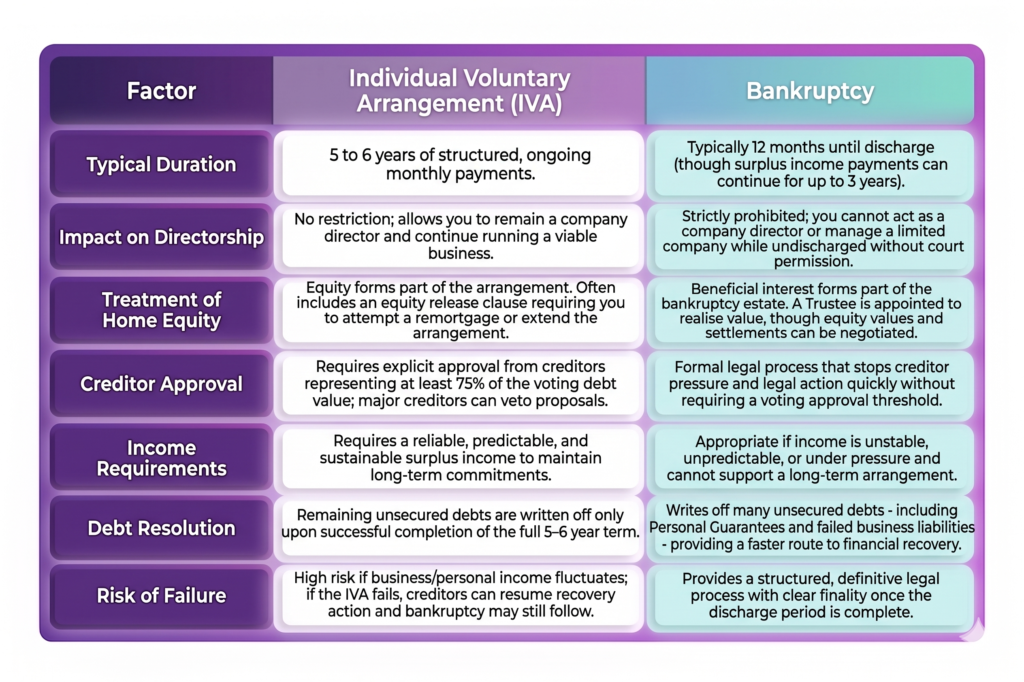

An Individual Voluntary Arrangement (IVA) is a formal agreement between you and your creditors to repay part of your debts over a fixed period, usually five or six years.

The arrangement is supervised by a licensed Insolvency Practitioner (IP). During the IVA, you make agreed monthly payments based on what you can realistically afford. In return, creditors agree to pause further enforcement action and, if the IVA completes successfully, any remaining unsecured debt included within the arrangement is usually written off.

For an IVA to be approved, creditors representing at least 75% of the voting debt value must agree to the proposal.

An IVA may be appropriate where:

- You have reliable and sustainable surplus income

- You want to avoid bankruptcy

- You need to remain a company director

- Your creditors are likely to support a structured repayment proposal

- You have assets that may be better protected through a formal arrangement

- You can realistically maintain payments for the full duration of the IVA

However, an IVA is not suitable in every situation and can become problematic where:

- Your income is unpredictable or already under pressure

- Your business is struggling or reliant on uncertain future trading

- The IVA proposal depends on optimistic financial forecasts

- A significant creditor is unlikely to support the arrangement

- Personal Guarantees or secured liabilities have not been fully assessed

- The IVA is being chosen primarily out of fear of bankruptcy, rather than long-term affordability

If an IVA fails, creditors can resume recovery action, and bankruptcy may still follow. This is why it is important that any IVA proposal is based on realistic affordability and a full understanding of your wider financial position.

Bankruptcy is a formal insolvency process available to individuals who are unable to repay their debts. In England and Wales, bankruptcy typically lasts for 12 months, although payments towards creditors can continue for up to three years if you have surplus disposable income through an Income Payments Agreement or Order.

Bankruptcy can write off many unsecured debts, including certain liabilities arising from failed businesses and Personal Guarantees. However, some debts are excluded, and secured creditors may still retain rights against secured assets, including property.

Once a bankruptcy order is made, a Trustee in Bankruptcy is appointed to review your financial affairs, assets, liabilities, income, and any available equity. Their role is to realise available assets for the benefit of creditors where appropriate.

Bankruptcy may be appropriate where:

- Personal Guarantee liabilities have become unmanageable

- The business has failed or is no longer financially viable

- Your income is too unstable to support an IVA or long-term repayment arrangement

- Creditor pressure and legal action need to be stopped quickly

- The overall debt level is unrealistic to repay within a reasonable timeframe

- You do not need to remain a company director in the immediate future

- There may be scope to negotiate property equity or settlements with the Trustee

Bankruptcy is a serious process and can affect:

- Your home and any available equity

- Your ability to act as a company director

- Your credit profile

- Certain assets and savings

- Your future borrowing position

However, bankruptcy is not always the outcome people fear most. In some situations, it can provide structure, certainty, legal protection from creditor action, and a realistic route toward financial recovery – particularly where ongoing repayment arrangements are no longer sustainable.

One of the biggest misconceptions we hear is:

“Bankruptcy means I lose everything.”

That is not how most real cases work.

In our experience, the main issue for many directors is not whether the trustee wants your everyday possessions. The real issue is your beneficial interest in property, business assets, surplus income and whether there is a sensible way to settle the trustee’s claim.

That is where strategy matters.

IVA vs Bankruptcy Cost Comparison:

One reason directors ask “is bankruptcy or IVA better?” is because the IVA can look easier at first glance.

Monthly payments may feel more manageable than bankruptcy. The word “arrangement” sounds less severe. And many people are told that an IVA protects their home.

But the real comparison is not emotional. It is financial.

You need to compare:

- Total IVA payments over five or six years

- IVA fees and supervisor costs

- Whether creditors are likely to approve the IVA

- What happens if your income drops

- What happens if the IVA fails

- Bankruptcy application costs

- Potential income payments in bankruptcy

- Property equity risk

- Trustee negotiation options

- Whether personal guarantees are fully dealt with

- How quickly you can rebuild afterwards

For directors, an IVA can become expensive if it is based on income that later disappears. A five or six-year commitment is a long time when your income depends on business performance.

By contrast, bankruptcy may be shorter, but it can involve asset risk. If you own a home, your beneficial interest may need to be valued and addressed. That does not automatically mean a forced sale, but it does mean the position needs expert review.

This is where many of our results come from.

Clients often approach us after being told bankruptcy would automatically mean losing the family home. In many cases, we have helped negotiate with trustees to reduce the amount required to settle the trustee’s interest, giving clients a realistic route to protect the property and move on.

In genuine client cases, we have seen situations where bankruptcy, combined with proper trustee negotiation, produced a better overall outcome than years of IVA payments. The reason is simple: the IVA cost was not just the monthly payment. It was the risk of paying for years, failing, and still facing bankruptcy later.

A fair IVA vs bankruptcy cost comparison should ask:

What will this cost me in money, time, risk and stress?

Not just:

What is the monthly payment?

“Will I Lose my Home with an IVA or Bankruptcy?”

This is one of the biggest questions people search for, and the honest answer is: not automatically.

But the risk must be taken seriously.

An IVA is often marketed as the safer option for homeowners. Sometimes it is. But an IVA does not make your home irrelevant. Depending on the terms, you may be expected to attempt equity release, extend the IVA if equity cannot be released, or make additional contributions.

Bankruptcy is different. If you own a property, your beneficial interest may form part of the bankruptcy estate. A trustee may seek to realise value for creditors.

That sounds frightening, but it is not the same as saying you automatically lose your home.

The important questions are:

- Is the property solely or jointly owned?

- What is the realistic market value?

- What is outstanding on the mortgage?

- What is your beneficial interest?

- Are there dependants or special family circumstances?

- What would a forced sale actually produce?

- What costs would a trustee incur?

- Is negotiation possible?

This is where generic IVA or bankruptcy advice often fails directors.

It treats home equity as a yes-or-no issue. In reality, it is often a negotiation issue.

Some clients come to us convinced their home is gone if they enter bankruptcy. They have read online forums, spoken to creditors, or been warned away from bankruptcy by someone selling an IVA. But once the figures are reviewed properly, the picture can look very different.

We have helped clients challenge inflated property assumptions, assess realistic equity, and negotiate with trustees. In some cases, clients have been able to protect the family home by settling the trustee’s interest for less than they feared.

That does not mean bankruptcy is risk-free. It is not.

But the myth that bankruptcy automatically means losing everything stops many directors from exploring a route that may actually produce a better, more commercial outcome.

If your home is at risk, you need specialist advice before choosing either route.

Useful guides:

Can I lose my home in bankruptcy?

Bankruptcy trustee negotiations

Case study: saving a used car dealer’s home

“Will Bankruptcy or an IVA Affect my Job?”

The answer to this question depends on your role, contract, profession and regulator.

For most employees, an IVA or bankruptcy may not automatically mean losing their job. But certain roles can be affected, especially where you work in finance, law, accountancy, regulated sectors, senior management, public office or positions of trust.

For directors, bankruptcy has a specific impact.

While undischarged, you cannot act as a company director or be involved in managing a limited company without court permission. That is one of the clearest reasons an IVA may appear better than bankruptcy for some business owners.

If your company is still viable, profitable and worth saving, an IVA or settlement strategy may help you avoid the director restrictions that come with bankruptcy.

But if the company has already failed, personal guarantees have been called in, and you no longer need to remain a director in the short term, the restriction may be less important than the debt solution itself.

This is where you need to be brutally honest.

Are you protecting a viable business, or are you protecting the title of ‘director’ after the business has already gone?

That distinction matters.

Many directors feel a strong emotional attachment to the company they built. That is understandable. But if the company can no longer trade, preserving the directorship may not be worth years of IVA payments.

The question should not be: Will bankruptcy affect my job?

The better question is: Does bankruptcy affect something I still need to preserve?

Myth-Busting Preconceptions Around IVAs and Bankruptcy

There are many myths around an IVA or bankruptcy. Some are harmless. Others cause directors to make expensive mistakes.

Myth 1: “An IVA is always better than bankruptcy”

No, it is not.

An IVA can be excellent where it is affordable, realistic and accepted by creditors. But a bad IVA can trap someone in years of payments before failing. For directors with personal guarantees, an IVA should never be chosen simply because bankruptcy sounds worse.

Myth 2: “Bankruptcy means losing everything”

This is one of the most damaging myths.

Bankruptcy is serious. Assets and property can be affected. But it does not mean someone turns up and takes everything you own. For many directors, the main issue is property equity, income and business interests, not ordinary household possessions.

Myth 3: “An IVA protects your home automatically”

Not necessarily.

An IVA may help avoid bankruptcy and can, in some cases, reduce the immediate risk to the family home. However, property equity often still forms part of the arrangement.

Many IVAs include an equity release clause, meaning you may later be asked to attempt to remortgage or introduce funds from your property. In some situations, restrictions or secured borrowing arrangements may also arise.

Importantly, if an IVA fails, creditors can resume recovery action and the risk to the property may return.

This is why it is essential to fully understand how your home is being treated within any proposed IVA before proceeding.

Myth 4: “Bankruptcy is only for people with no assets”

Incorrect.

Many individuals who enter bankruptcy do have assets, including equity in property. Bankruptcy is not reserved solely for people with “nothing left”.

The key issue is not simply whether assets exist, but how those assets are assessed, managed, and potentially negotiated within the process.

In some situations, bankruptcy can still represent the most commercially realistic option — particularly where debts are unmanageable, income is unstable, or long-term repayment proposals are unlikely to succeed.

We have worked with clients who owned property and still achieved better overall outcomes through bankruptcy and structured trustee negotiation than they would have through a long-term IVA arrangement.

Every case is different. What matters is understanding the full picture before making a decision driven by fear or assumption.

Myth 5: “An IVA is better for your credit rating”

This is often oversimplified.

Both an IVA and bankruptcy are formal insolvency procedures, and both can have a significant impact on your credit profile, future borrowing ability, mortgage applications, insurance, and access to business finance.

An IVA should not automatically be viewed as the “credit-friendly” option simply because bankruptcy sounds more severe.

In practice, the better question is:

Which solution is realistically sustainable, and which leaves you in a stronger long-term financial position once the process is complete?

For some people, a five or six-year IVA that ultimately fails can cause more prolonged financial pressure than a shorter bankruptcy process that provides a clearer route to recovery.

The right solution depends on your income, assets, liabilities, business position, and long-term objectives, not simply how the procedure is perceived publicly.

Myth 6: “Creditors will accept any IVA proposal”

Incorrect.

An IVA is not automatically approved simply because it has been proposed.

Creditors vote on whether to accept the arrangement, and voting power is based on the value of the debt owed. For an IVA to be approved, creditors representing at least 75% of the voting debt value must agree to it.

This means that a single major creditor can have significant influence over the outcome.

Where liabilities involve:

- Business lenders

- HMRC

- Personal Guarantees

- Commercial finance providers

The proposal may face greater scrutiny, particularly if creditors believe the repayment offer is unrealistic or unsupported by the wider financial position.

This is why the quality of the proposal matters. An IVA built on overly optimistic income forecasts or unsupported assumptions is far less likely to succeed long term.

Myth 7: “Bankruptcy lasts forever”

No.

In England and Wales, bankruptcy usually lasts for 12 months, after which most individuals are discharged from the process. However, some effects can continue beyond discharge.

For example:

- Bankruptcy remains on your credit file for six years

- Certain professional or borrowing restrictions may continue

- And if you have surplus income, you may be required to make payments under an Income Payments Agreement or Order for up to three years

That said, for some directors and business owners, a shorter and more defined bankruptcy process may be more realistic than committing to five or six years of IVA payments that may become unsustainable over time.

The key consideration is not simply how long the process lasts, but whether the proposed solution is genuinely affordable, achievable, and capable of improving your long-term financial position.

Myth 8: “You should avoid bankruptcy at all costs”

This is one of the most damaging misconceptions surrounding insolvency.

Bankruptcy is a serious legal process and should never be entered into without fully understanding the consequences. However, avoiding bankruptcy purely because of fear, stigma, or misunderstanding can sometimes lead to greater financial and personal damage over time.

We regularly speak to people who have:

- Exhausted savings trying to maintain unsustainable repayments

- Refinanced property repeatedly

- Taken on additional borrowing

- Or entered long-term arrangements that ultimately failed, simply because they believed bankruptcy must be avoided at all costs.

In some cases, that approach can increase stress, prolong creditor pressure, and worsen the overall financial outcome.

The objective should not be to avoid a particular word or procedure.

The objective should be to identify the solution that is most realistic, sustainable, and commercially sensible for your circumstances.

The Truth No One Else Will Tell You

Here is the reality.

An IVA is not automatically the “safe” option.

And bankruptcy is not automatically the disaster many people fear.

For directors dealing with Personal Guarantees, business debts, creditor pressure, or concerns around the family home, this decision should never be based on generic debt advice or assumptions about which process “sounds better”.

The right solution depends on the full picture:

- Your business position

- Your income and affordability

- Your assets and home equity

- The type of creditors involved

- And your long-term objectives

We regularly speak to directors who were initially told that an IVA was their only sensible option. But once the figures, creditor position, and wider risks were properly reviewed, bankruptcy combined with trustee negotiation ultimately provided a more practical and financially sustainable route.

Equally, we have also supported clients where an IVA, settlement strategy, or negotiated repayment arrangement was the right way to protect a directorship, preserve assets, and avoid unnecessary escalation.

That is the key point:

There is no universal answer.

What matters is identifying the route that produces the strongest long-term outcome for your specific circumstances.

One of the most common things our clients tell us is:

“I wish I had spoken to you sooner.”

Often before:

- Agreeing to unaffordable repayment arrangements

- Assuming bankruptcy meant losing everything

- Refinancing unnecessarily

- Or allowing creditor pressure to dictate major decisions

If you are a director dealing with:

- Personal Guarantees

- Business borrowing

- HMRC pressure

- Home equity concerns

- Or wider personal exposure, it is important to obtain advice that fully considers both the business and personal implications of the situation.

At Bell & Company, we regularly assist clients with:

- IVA vs bankruptcy assessments

- Personal Guarantee exposure

- Trustee negotiations

- Director liability issues

- Home equity risk

- Creditor settlement negotiations

- Post-insolvency strategy and protection

Free debt advice services such as StepChange and Citizens Advice can be extremely valuable for straightforward personal debt matters. However, where the situation involves business borrowing, Personal Guarantees, director exposure, or significant assets, more specialist strategic advice may be required.

The question is not simply:

“Which is better an IVA or bankruptcy?”

The real question is:

“Which route leaves you in the strongest position moving forward?”

That is where the right advice can make all the difference.