Every day, we speak with business owners who are navigating the pressures of statutory demands, personal guarantee exposure, and increasing creditor action. What often makes the situation harder is not just the financial strain, but the absence of clear, straightforward information about their options.

When your livelihood – and often your family home – is at stake, reassurance alone isn’t enough. You need clear, practical information you can rely on.

Drawing on our experience supporting businesses through millions of pounds worth of debt matters, here are the five questions we hear most often — and the straightforward answers directors need.

1. “What if a deal can’t be reached?”

A common fear is that a failed negotiation leaves you in a worse position. Our approach is rooted in a 100% success rate on the cases we accept. This isn’t because we have a magic wand; it’s because we are selective and strategic.

- The Selective Approach: We only take on cases where we are confident a successful resolution is possible.

- The “Pivot” Strategy: We are appointed until full resolution, not just the first “no.” If Plan A (a lump sum settlement) is rejected, we immediately pivot to Plan B: structured payment plans, bankruptcy protection, or alternative mediation.

- Persistent Representation: We don’t walk away when things get difficult. We stay in the room until a commercial settlement is reached.

2. “What happens if I just ignore this?”

We understand the temptation. When a debt letter arrives, the “ostrich effect” is a natural human response. However, in the UK legal system, silence is seen as admission.

Ignoring the problem creates a predictable, downward trajectory:

- Weeks 1–4: Escalation of letters, compounding interest (often 8%+), and late fees.

- Months 2–3: County Court claims and Statutory Demands are served.

- Months 4–6: CCJs are registered; creditors apply for Charging Orders against your property.

- Months 6–12: Bankruptcy petitions are filed; forced sale proceedings begin.

- 12 Months+: High Court Enforcement (Bailiffs) and potential repossession.

The Bottom Line: The sooner you act, the more leverage you have.

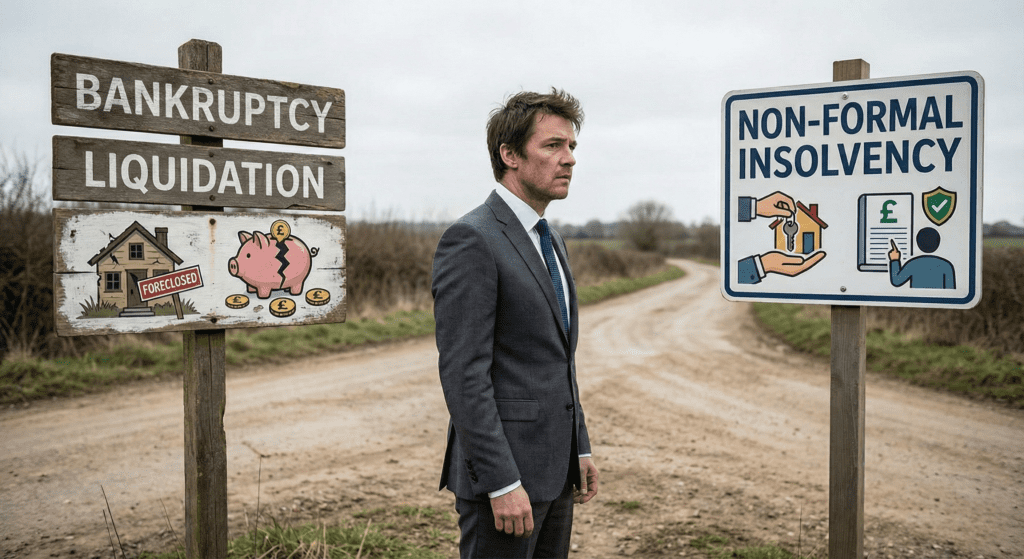

3. “Can creditors really take my house?”

In certain circumstances, yes – but it is rarely quick or automatic. There is a structured legal process a creditor must follow before they can seek to enforce against property, and each stage involves specific criteria and court oversight.

What creditors may be able to do (depending on the circumstances):

- Obtain a County Court Judgment (CCJ).

- Apply for a Charging Order, which can secure the debt against a property.

- In more serious cases, apply to the court for an Order for Sale.

Each step is subject to legal thresholds and, in many cases, judicial discretion. It is not an immediate “one-step” process.

How we protect you:

- Early Intervention: Responding promptly to statutory demands or court action can prevent matters from escalating unnecessarily.

- Negotiation and Settlement: Engaging creditors early can often lead to structured repayment or settlement before security is sought over property.

- Strategic Planning: Where enforcement risk is real, careful planning can help ensure that any decisions taken protect as much equity and stability as possible, rather than leaving matters to unfold under pressure.

4. “I just received a Statutory Demand. How much time do I have?”

A Statutory Demand is a formal legal notice served by a creditor. While it is a serious step and can be a precursor to bankruptcy proceedings, it is not necessarily a “point of no return.” There are strict time limits and specific options available once it has been served, and early action can be critical in determining what happens next.

- The 18-Day Rule: You have 18 days from service of the Statutory Demand to apply to the court to have it set aside, if there are valid grounds to do so.

- The 21-Day Rule: If the demand is not resolved, secured, or successfully challenged within 21 days, the creditor may then present a bankruptcy petition.

When a client approaches us with a Statutory Demand, we act quickly to assess whether there are grounds to challenge it and, where appropriate, prepare the necessary application within the strict time limits. At the same time, we contact the creditor or their solicitors to request a temporary hold on further action while discussions are ongoing.

In many cases, creditors are willing to pause proceedings to allow for constructive dialogue, creating valuable breathing space to explore settlement or repayment options without the immediate escalation to court.

5. “How much can you actually negotiate this down?”

Settlement discussions are rarely just about the headline balance owed – they are usually shaped by what is realistically recoverable in practice. Creditors tend to take a commercial view, weighing the certainty of an agreed payment now against the cost, delay and uncertainty of formal enforcement action.

In negotiations, it is important to present a clear and evidenced picture of the overall circumstances – including financial position, asset profile, other liabilities, and any relevant personal factors. When properly articulated, this broader context can support a pragmatic resolution that reflects commercial reality and is in both parties’ interests.

Real Outcomes from our Case Studies:

- Retail Director: Faced a £183,000 PG demand from an aggressive FinTech lender. We negotiated this down to £63,000, a saving of over £120,000.

- Property Shortfall: A client was left with a £170,000 shortfall after a forced sale. We resolved the entire debt for just 6% of the original amount, allowing them to remain bankruptcy-free.

- Construction Sector: Facing £600,000 in total debt, we secured an 85% reduction, settling for £90,000 and protecting the family home.

Read more case studies.

What Happens During a Free Consultation?

Taking the first step is often the hardest part. When you book a strategy call with us, here is what you get:

- A Situation Audit: We review your specific creditors (HMRC, Banks, FinTechs) and your personal exposure.

- Realistic Expectations: We provide a transparent settlement range, timelines and our costs.

- No Pressure: We explain your options clearly. You decide how to proceed.

Take Back Control of Your Future

This problem won’t resolve itself, but it is resolvable. Don’t let a personal guarantee or a statutory demand define your future. Speak to the UK’s leading debt strategists today.

Book Your Free Debt Strategy Consultation. Get a confidential assessment from a senior consultant and start your journey from fear to freedom.